Reader RW had the following comments in regards to re-entering the market given the close proximity of the domestic TTI (Trend Tracking Index) to bear market territory:

Reader RW had the following comments in regards to re-entering the market given the close proximity of the domestic TTI (Trend Tracking Index) to bear market territory:

Could you clarify something for me? The domestic trend is still a little positive but you are out of all domestic ETF/Mutual Funds. Is that because each that you were invested in has already lost their 7% to exit and your trend line merely tells you whether you can invest in others. That distinction is a bit unclear.

In addition, hypothetically, since the line is still positive (but everyone is waiting/considering it will turn negative shortly) and the market find a bottom now, there will not be a clear example to get back in long. How do you handle a trading range that hovers around the trend line indicator?

In other words there is no cow bell when to get back in. This to me is the real weakness in this strategy if a person was really attempting to go it alone. Perhaps a daily blog could be used on the subject in general/or examples/or particulars.

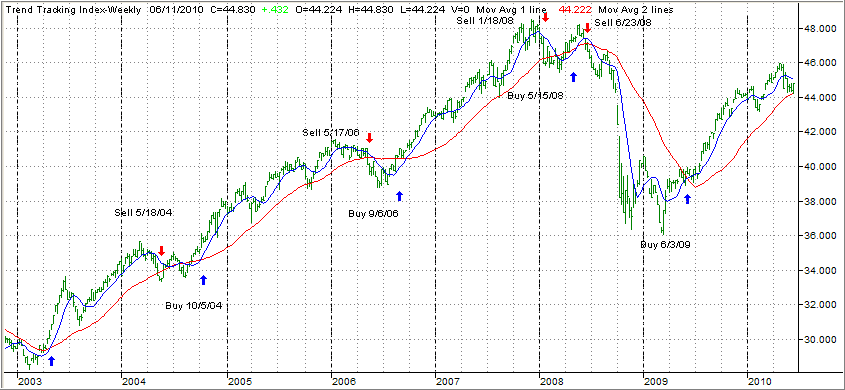

There were many discussions about this topic during a variety of blog posts along with reader Q&As; last year. A good reference is the 70-page PDF file that covers the sell stop topics and more. If you missed it, you can download a free copy here.

While we were, during last year’s discussion, not within striking distance of heading into bear market territory, the principles discussed nevertheless did not change.

In “Deploying Stopped Out Money” I said:

Depending on your risk aversion, you could wait until the funds/ETFs, you’ve been stopped out of, take out their old highs before re-entering.

To be clear, whenever markets go through a directional shift accompanied by huge volatility, and you get stopped out, you will always find yourselves a little bit in no man’s land. You have to realize that no investment approach will always give you a perfect answer to any scenario allowing you to simply wait for the cow bells to alert you to your next move.

The overriding purpose for using stop losses is to limit downside risk should the markets head south in a big time a la 2008. While the jury is still out as to whether that will happen or not, you will now have to wait for the markets to resume their primary trend (up or down).

Over the past couple of trading days, we have bounced successfully off the trend line. If you are an aggressive investor, you could jump in now realizing that, if you get whipsawed again, your downside risk may only be some 3% or less before the trend line gets broken and an all-out sell signal is being generated.

Personally, I prefer to wait for a clearer signal and better upward momentum before making a new commitment.

Let’s take a look at some real numbers using the widely held SPY as an example. Here’s how it played out for one client, who came aboard in March 2010:

We purchased SPY on 3/16/10 for 116.41; the high price occurred in April at 121.81, after which the markets slid with the sell stop being triggered and executed on 5/19/10 at 112.08 for a loss of -3.72%.

Last Friday, after a strong 2-day rally, SPY closed at 109.68, which is -2.14% below our sales price of 112.08.

Not only that, SPY is still showing weakness by having moved below its own long-term trend line by -1.35% with all momentum numbers being negative across the board (4-wk, 8-wk, 12-wk, YTD).

A purchase of SPY now given these circumstances would amount to nothing more than bottom fishing. While you may get lucky, the numbers are not in your favor. You want to pick a spot at which time SPY has risen sufficiently to put the odds of continued upward momentum on your side.

While there are never any guarantees, I have found that once the old high (in this example 121.81) has been taken out again, that price level would represent the clearest sign that bullish momentum has returned. That’s a long way to go, however, and investors on balance are not a patient bunch.

An earlier entry point that I have tested, would be a percentage above your stopped out price, which in this case was 112.08. I have had good success in back tests using a re-entry point of 3% above that level, which would be around 115.44.

As I have pointed out, volatility is the greatest during transitional periods from bullish to bearish as opposing forces seem to be in a constant tug-of-war at that period in time.

My view therefore is that I’d rather be a little bit late with re-entering by possibly avoiding another whip-saw signal.

After all, being late to a bullish party will merely reduce your potential profits while being late when the bear strikes could cut deeply into your principal. Remember the losses of the last decade?