ETF Tracker Newsletter For July 24, 2026

ETF Tracker StatSheet

You can view the latest version here.

CHIP STOCKS SINK NASDAQ AS GEOPOLITICAL RISKS RATTLE MARKETS

- Moving the market

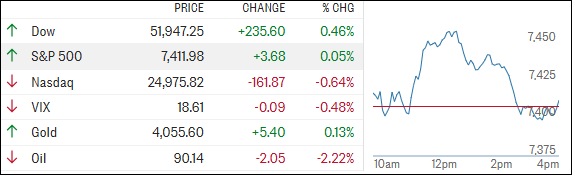

It was a challenging end to the week for the major indexes, with the Nasdaq once again taking the brunt of the selling pressure as weakness in semiconductor stocks weighed heavily on the tech sector.

Chip stocks got off to a shaky start after Intel initially rallied on better-than-expected second-quarter results, only to reverse course and finish down 4%.

The selling spread across the sector, with Broadcom and AMD each losing 2%, Micron dropping 6%, and the VanEck Semiconductor ETF (SMH) falling 2%. After months of leading the market higher, semiconductors found themselves firmly in the crosshairs.

The broader market remained on edge following Thursday’s selloff, when the Dow tumbled more than 500 points and both the S&P 500 and Nasdaq suffered their largest one-day declines since late June.

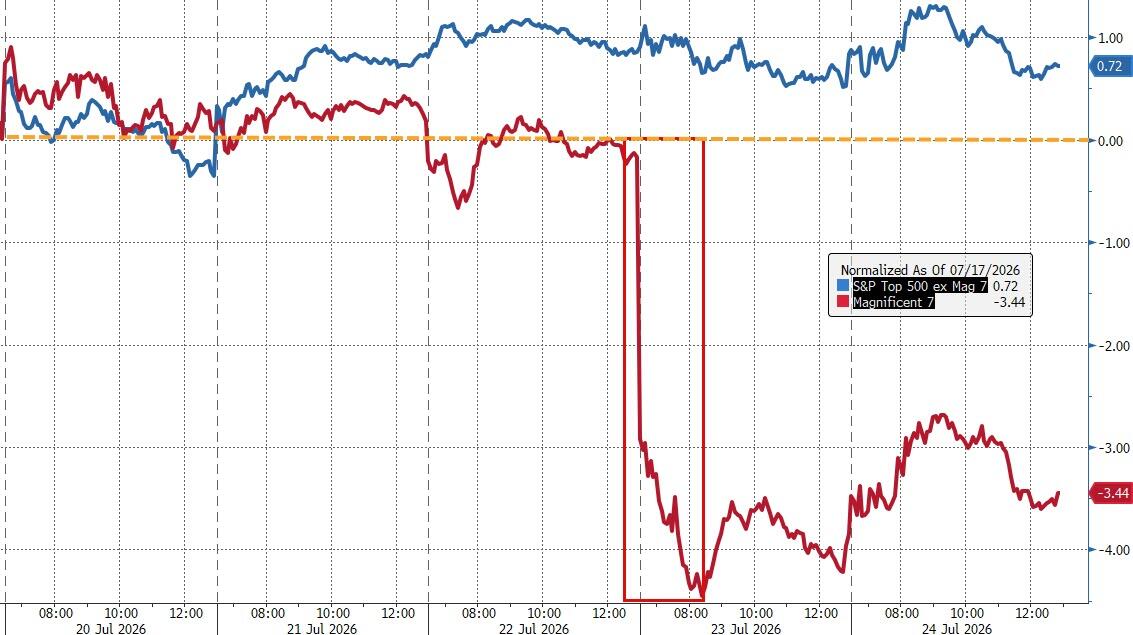

Disappointing reactions to earnings from Tesla and Alphabet have raised questions about whether the market’s biggest winners can continue carrying the rally.

Adding to investor unease were rising geopolitical tensions in the Middle East. President Trump indicated he is considering a major military response against Iran as the conflict continues to expand into the Red Sea region.

Markets dislike uncertainty, and right now traders are being forced to react to a constant stream of geopolitical headlines that can change sentiment in a matter of minutes.

By the closing bell, the Dow managed to stay in positive territory, while the S&P 500 finished little changed.

The Nasdaq, however, ended lower under the weight of chip stocks. For the week, all three major indexes finished in the red, with the Mag 7 notably underperforming the rest of the market.

{kind=link}

Outside of equities, bond yields moved higher alongside oil prices, while the dollar posted its strongest weekly performance in more than a month.

{kind=link}

{kind=link}

Gold recovered to finish above $4,000 an ounce, although well below its intraday highs. Bitcoin briefly tested its mid-June highs before fading and ending the session roughly flat.

{kind=link}

{kind=link}

One development that may deserve more attention is the growing disruption to global shipping routes in the Middle East. Traffic through the Strait of Hormuz has slowed dramatically as tensions in and around the Persian Gulf intensify.

With only six ships passing through the strait on Thursday, the lowest level since early May, the potential impact on energy markets and future oil prices is becoming harder to ignore.

With earnings season losing some momentum, geopolitical risks rising, and markets increasingly reacting to each new headline, the key question remains: Can traders keep their confidence in stocks, or is a more cautious stance beginning to make sense?

Read More