- Moving the market

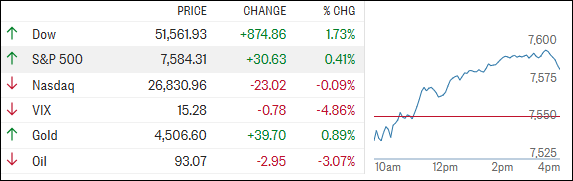

Stocks started the day on a stronger footing, with chip names leading the rebound after Friday’s brutal sell-off. Traders seemed eager to step back in, hoping the recent weakness was just a reset rather than the start of something bigger.

Micron, which has been a key driver of this latest bull run, jumped nearly 10% after getting hit hard on Friday. Nvidia and Broadcom also bounced back, helping lift sentiment across the tech space.

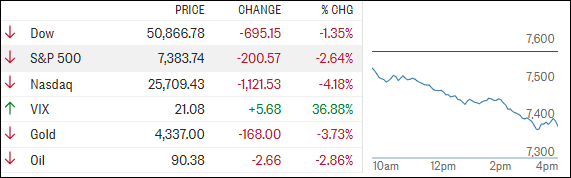

But the backdrop remains anything but calm. Fresh strikes by Iran over the weekend raised new concerns about whether the already fragile ceasefire can hold. The situation escalated after Iranian Parliament Speaker Ghalibaf accused the U.S. of violating agreements, pointing to actions like the naval blockade.

Tensions kept energy markets on edge. Oil prices moved higher after Israel launched what it described as a “large-scale strike on strategic defense systems” in response to Iranian attacks.

Despite the back-and-forth, President Trump said both sides are still pushing toward an immediate ceasefire and urged them to halt hostilities altogether.

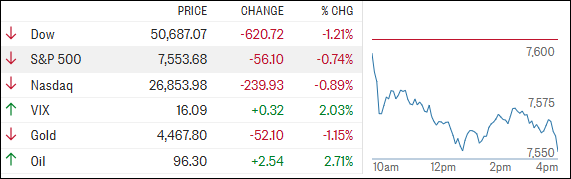

Meanwhile, one analyst pointed out that the market might be running into a different kind of problem—its own success. After a strong comeback, lingering inflation risks are still hanging over investors’ heads and could limit how far this rally can go.

Looking ahead, it’s shaping up to be a big week. Inflation data will be front and center, along with the highly anticipated public debut of Elon Musk’s SpaceX. It’s expected to be one of the largest IPOs ever and could serve as a major test for the current AI-driven market optimism.

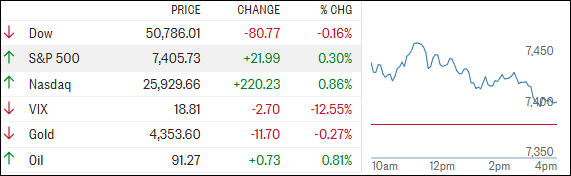

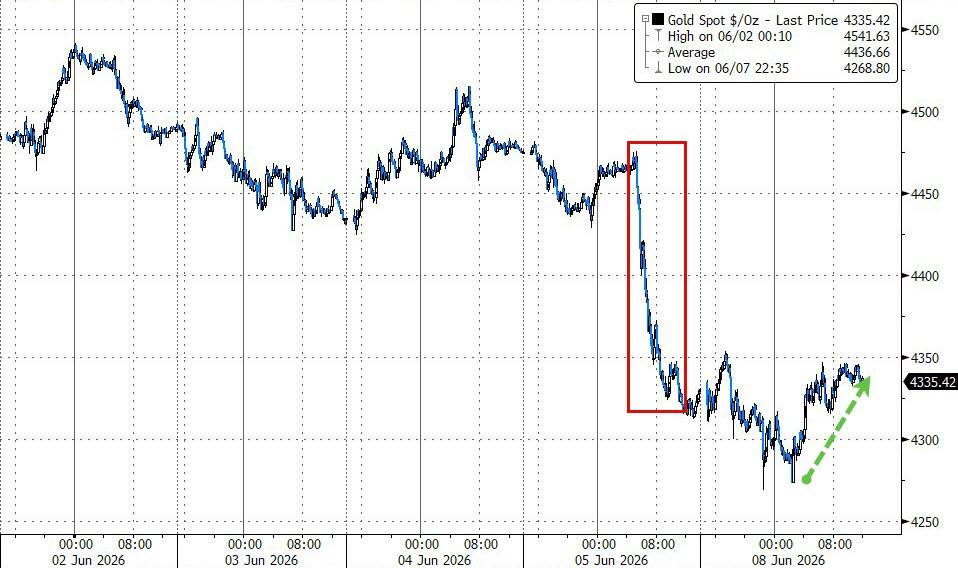

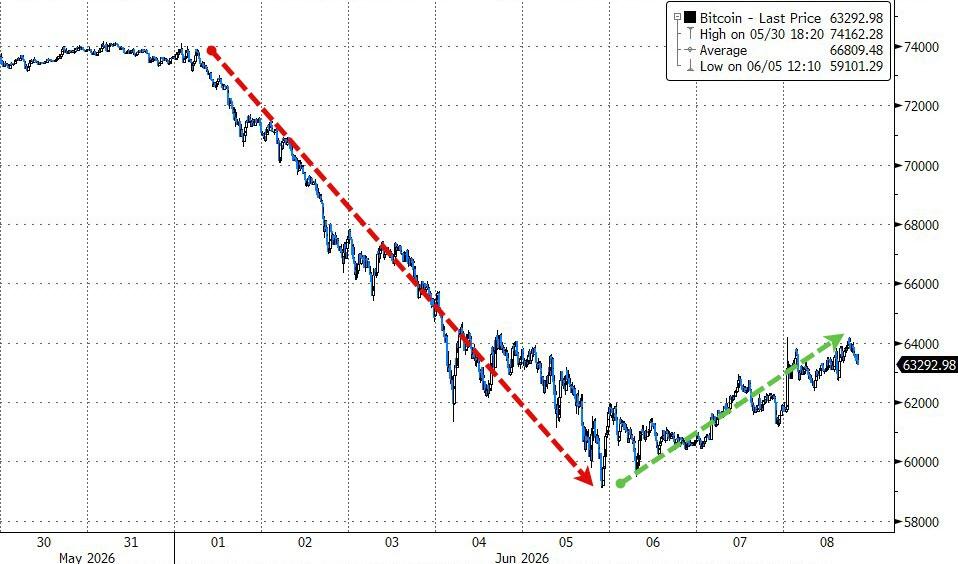

By the close, the S&P 500 and Nasdaq managed to recover a portion of Friday’s losses—more of a relief rally than a full recovery. Bond yields ticked higher, while the dollar slipped slightly, giving gold a lift after an earlier dip. Bitcoin also bounced back, testing the $64K level.

So now the big question: was this just a classic dead-cat bounce, or the start of a more durable move higher?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}