ETF Tracker StatSheet

https://theetfbully.com/2017/09/weekly-statsheet-etf-tracker-newsletter-updated-09142017/

MISSION ACCOMPLISHED: S&P 500 CONQUERS ITS 2,500 LEVEL

- Moving the Markets

As we have become accustomed to, news reports, that should affect markets negatively, were ignored as the major indexes continued relentlessly higher with the S&P managing, at the very last minute, to close above its 2,500 marker for the first time.

The latest N. Korean missile test was shoved aside as were economic reports that were anything but comforting. First, there were retail sales, which tumbled in August -0.2% MoM with, surprisingly, online sales slumping. At the same time, July’s gains were revised and cut in half. The August industrial production numbers crashed the most since May 2009 as auto sales collapsed. Completing the trifecta of bad reports was a slipping consumer confidence index.

ZH summed up this week best:

- Hurricane Irma crushes Florida

- North Korea test fires ICBMs across Japan (again)

- Economic data misses across the globe (China and US most notably)

- Terrorism in UK and France

And the result – drum roll please – new record highs for the Dow, the S&P, and the Nasdaq… with the Dow’s best week of the year! Go figure…

In ETF space, Semiconductors (SMH) took top billing today by gaining +1.32% with Emerging Markets (SCHE) occupying a distant 2nd place with +0.70%. On the downside, we saw only one red number and that was Transportations (IYT), which lost -2.00%.

Interest rates ended the day unchanged, gold slipped again, and the US dollar (UUP) lost -0.33% on the day but managed to eke out a gain for the week. Nevertheless, its YTD downtrend remains intact, and the loss is now over 11%.

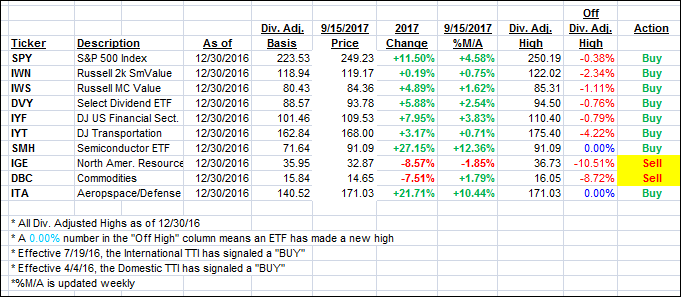

- ETFs in the Spotlight (updated for 2017)

In case you missed the announcement and description of this section, you can read it here again.

It features 10 broadly diversified and sector ETFs from my HighVolume list as posted every Saturday. Furthermore, they are screened for the lowest MaxDD% number meaning they have been showing better resistance to temporary sell offs than all others over the past year.

The below table simply demonstrates the magnitude with which some of the ETFs are fluctuating in regards to their positions above or below their respective individual trend lines (%M/A). A break below, represented by a negative number, shows weakness, while a break above, represented by a positive percentage, shows strength.

For hundreds of ETF choices, be sure to reference Thursday’s StatSheet.

Year to date, here’s how the 2017 candidates have fared so far:

Again, the %M/A column above shows the position of the various ETFs in relation to their respective long term trend lines, while the trailing sell stops are being tracked in the “Off High” column. The “Action” column will signal a “Sell” once the -7.5% point has been taken out in the “Off High” column.

- Trend Tracking Indexes (TTIs)

Our Trend Tracking Indexes (TTIs) slipped a tad (due to the recalculation of the M/A), as the major indexes continued their northerly climb.

Here’s how we closed 9/15/2017:

Domestic TTI: +2.69% (last close +2.77%)—Buy signal effective 4/4/2016

International TTI: +6.85% (last close +7.20%)—Buy signal effective 7/19/2016

Disclosure: I am obliged to inform you that I, as well as my advisory clients, own some of the ETFs listed in the above table. Furthermore, they do not represent a specific investment recommendation for you, they merely show which ETFs from the universe I track are falling within the guidelines specified.

————————————————————-

READER Q & A FOR THE WEEK

All Reader Q & A’s are listed at our web site!

Check it out at:

https://theetfbully.com/questions-answers/

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly or get more details at:

https://theetfbully.com/personal-investment-management/

———————————————————

Back issues of the ETF/No Load Fund Tracker are available on the web at:

https://theetfbully.com/newsletter-archives/

Contact Ulli