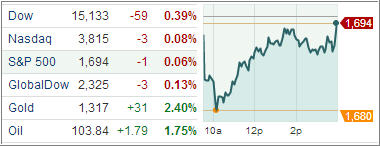

U.S. equities ended slightly in the red after spending most of the session in a steady climb off the opening low, as domestic markets erased chunks of yesterday’s gains during the second day of the partial government shutdown.

Adding to worries is the report of a disappointing private sector job growth, which could be the only piece of September payroll data we get this week amid the government shutdown. Treasuries were higher in the wake of the employment data, as well as a dip in weekly domestic mortgage applications.

The shutdown fight is rapidly merging with a higher-stakes battle over the government’s borrowing power that is expected to come to a head soon. Many analysts believe that the longer the shutdown goes on, and the more headlines shift towards the October 17 deadline, investors are becoming more and more concerned. A partial shutdown lasting one week would probably shave 0.1 percentage point from economic growth, according to the median estimate of economists, with the costs accelerating if the closing persists.

The Nasdaq (-0.1%) and the S&P were able to regain the bulk of their losses while the Dow (-0.4%) trailed throughout the session. Six of ten sectors finished in the red with energy (+0.3%) ending in the lead as crude oil advanced 1.8% to $103.89 per barrel. Another commodity-related sector, materials (+0.2%), also finished ahead of the broader market as steelmakers and miners contributed to the relative strength.

The European equity markets moved to the downside as the U.S. fiscal impasse, exacerbated by the nearing debt ceiling deadline, worried traders. Meanwhile, the European Central Bank left its benchmark interest rate unchanged at a record low of 0.50%, as widely expected. The ECB also kept its deposit rate at zero.

Elsewhere, stocks in Asia finished mixed as traders continued to grapple with the impact of the government shutdown and the looming debt ceiling deadline in the US. Meanwhile, volume remained muted as markets in mainland China and India were closed for holidays.

Our Trend Tracking Indexes (TTIs) closed fractionally lower ending the day at +3.35% (Domestic TTI) and +6.76% (International TTI).

Contact Ulli