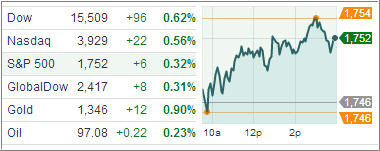

Domestic equity ETFs closed the trading session nicely higher, putting the Standard & Poor’s 500 Index three points from a record, in the wake of a stronger-than-forecasted read on Chinese manufacturing activity and as another plethora of earnings reports flooded the Street.

Treasuries were slightly lower following a report that showed initial weekly jobless claims came in above expectations, while the domestic trade deficit came in narrower than anticipated. In other economic news, a preliminary read on October manufacturing activity came in below expectations, while regional manufacturing growth surprisingly accelerated. Elsewhere, the U.S. dollar was nearly unchanged, while gold and crude oil prices were higher.

On the equity front, Ford Motor posted better-than-expected profits and upbeat guidance, while Dow members AT&T and 3M reported earnings that were slightly above analysts’ forecasts. Moreover, Dow Chemical missed forecasts and Symantec Corp reported disappointing revenues and guidance. Outside of some choppy action during the first hour, equity indices climbed steadily throughout the session.

The Dow led from the start. Meanwhile, the broader industrial sector (+0.7%) finished among the leaders as transports contributed to the strength. The Dow Jones Transportation Average gained 0.9% with airlines leading the pack.

Elsewhere, the discretionary sector (+1.0%) also provided leadership as homebuilders rallied. The broader iShares US Home Construction ETF jumped 2.8%. In addition to builders, carmakers also underpinned the sector. While five of six cyclical groups ended with solid gains between 0.5% and 1.0%, the financial sector could not make a sustained move into positive territory until the final hour.

The group added just 0.1% after spending the entire session just below its flat line. On the downside, all four countercyclical groups posted losses. Health care ended just below its flat line while consumer staples (-0.2%) and utilities (-0.2%) registered modest declines. The telecom services space (-1.0%) was the weakest sector of the day, pressured by shares of AT&T after the telecom giant reported a one-cent beat on revenue just below analyst estimates.

Elsewhere, Chinese manufacturing output reported favorable read. China’s HSBC/Markit Flash Manufacturing PMI Index increased to 50.9 for October, from 50.2 in September, compared to the 50.4 level that economists had expected.

Our Trend Tracking Indexes (TTIs) recoverd from yesterday’s pullback and closed higher with the Domestic TTI ending at +5.11%, while the International TTI settled at +9.11%.

Contact Ulli