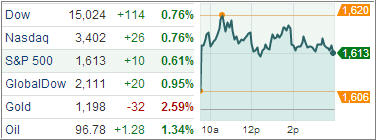

U.S. stocks climbed for a third straight day today, allowing the Dow Jones Industrial Average to close above 15,000 again and sending the Standard & Poor’s 500 Index to its biggest three-day rally since January.

Several Federal Reserve policymakers threw a big assist by jawboning the markets higher with comments that the central bank is not likely to pare its stimulus before the economy is ready. The Dow rose 114 points (0.8%) to 15,025, the S&P 500 Index added 10 points (0.6%) to 1,613, while the Nasdaq Composite gained 26 points (0.8%) to 3,402.

On economic news, personal income rose 0.5% in May, the most in three months, and above the consensus of 0.2%. Real disposable personal income rose 0.4% and is up 1.0% on a y/y trend basis. While this is below the average 2.7% gain per annum, it is allegedly supportive of stable growth in real consumer spending.

Personal consumption expenditures (PCE) rebounded 0.3%, in line with the consensus, led by a 0.9% gain in durables, the most this year. Real PCE rose 0.2%, but continues to perform below average at this stage of the expansion.

Meanwhile, Initial claims for unemployment insurance fell 9,000 to 346,000 last week, near the consensus of 345,000. The previous week was revised up by 1,000 to 355,000. The four-week average of claims fell 2,750 to 345,750, and is consistent with moderate payrolls growth.

Equities were off to the races at the sound of the opening bell, aided by today’s economic upbeat numbers. Nine of 10 industries in the S&P 500 Index advanced. Stocks received a secondary boost from the pending home sales report as May sales rose 6.7% (1.5% consensus). Today’s housing data provided homebuilders with a significant boost.

Most other cyclical groups also registered solid gains with financials settling in the lead, sporting a gain of 1.3%. Telecom space ended higher by 0.9% to extend its June advance to 2.6%. Meanwhile, the second-best sector of the month, consumer staples, climbed 0.9%, padding its June return to 0.4%.

On the downside, materials shed 0.1%. The sector was pressured by a 2.1% loss in Monsanto. Gold continued its weakness, as futures slumped 2.6% to $1198.00 per troy ounce. This marked the first time the yellow metal traded south of the 1200 level since August 2010. Treasuries saw some intraday weakness but ended near their highs after today’s strong 7-yr auction. The benchmark 10-yr yield slipped six basis points to 2.511%.

As a result of this 3-day rebound, our Trend Tracking Indexes (TTIs) headed higher as well with the Domestic TTI ending at +1.18%, while the International TTI closed at +3.34%.

Contact Ulli